Unless you’ve been living under a pretty sizable rock, you’ve already heard about Bitcoin.

Perhaps you’ve heard that it’s the currency of choice for drug dealers and criminals. Or you’ve heard that it uses as much energy as entire countries. Perhaps you’ve read about someone who bought Bitcoin way back in the day, only to lose their backup, losing millions and millions of dollars in the process.

But, more likely than not, you’re among the 90% of people who haven’t really paid much attention to “that Bitcoin thing” yet. Perhaps, you’re not sure what the big deal is, and at this point, you’re too afraid to ask.

Perhaps you believe that Bitcoin is “nerd money,” “a bubble,” or just not something you’re interested in.

In this article, my goal is to change your mind.

Why do I care? Because like most people who’ve studied Bitcoin for a few years, I wholeheartedly believe that this technology is going to change the course of human history for the better. I know, beyond a shadow of a doubt, that Bitcoin is one of the most important inventions humanity has ever created. What’s more, I know that like the internet, you cannot simply “opt out” of a technology that transforms society. You can be a late adopter — at your own peril — but you cannot opt out. And the sooner that everyday people understand all this, the better. As my friend David explains, “if you hold any currency, you have already placed a bet regarding Bitcoin — and if you don’t know what it is, then you have bet against it.”

This article is not going to get too deep into the technology of Bitcoin, because quite frankly, you don’t need to understand it any more than you understand TCP/IP or how the internet actually works. Instead, whether or not you’re a “tech person,” understand the history of money, or have a basic grasp of economics, my goal is to simplify the tangible benefits of Bitcoin so that anyone can understand them. What you do with that information is up to you. But at least you won’t find yourself saying “If only I’d known…”

So come one, come all. Beginner Bitcoiners and technophobes. Gather round, while a die-hard Bitcoiner explains…

What’s the big deal with Bitcoin, anyways?

1. The fiat money system is broken (Government-issued money sucks)

As a form of money, the idea of “fiat” money is a relatively new concept. Throughout history, humans have used different objects or substances as “money,” but it was only recently that this money became what we would call “fiat.” (“Fiat,” in Latin, means “it shall be,” and reflects the idea that fiat money is only valuable because governments declare it to be). Money is a technology almost as old as human societies, and it existed way before empires and governments. Money, therefore is not only whatever a government says is money, but any good with certain properties that make it suitable as a medium of exchange. The idea of having a form of money backed by a government or central bank is actually pretty new.

Up until the 1930’s (and then, conclusively, in 1971), the US dollar and many other currencies were actually based on something: they were tied to Gold. This meant that you could, at least theoretically, redeem your dollars for gold, if you wanted to. In this way, the US dollar and other currencies had certain limits around them. Except for brief periods where governments abandoned the gold standard, they couldn’t just print more money willy-nilly.

Today, however, there is no limit to how much money can be printed. Governments around the world are indebted by a total of $281 trillion dollars — an amount that they literally will never be able to pay.

To keep up with their debts, and to pay for various projects, governments (and the privately-held central banks that loan to them) maintain a monopoly on the ability to print more money. (In reality, they don’t even have to print money, they just tell banks to lend more to people, effectively creating more money out of thin air, with no cost to them whatsoever).

Although this “quantitative easing” (printing money to flush the market with cash) is presented to us as a way to “manage and balance the economy,” in reality, it presents a lot of problems. First of all, through continuous inflation, governments are able to slowly drain the savings of everyday people to absolutely nothing.

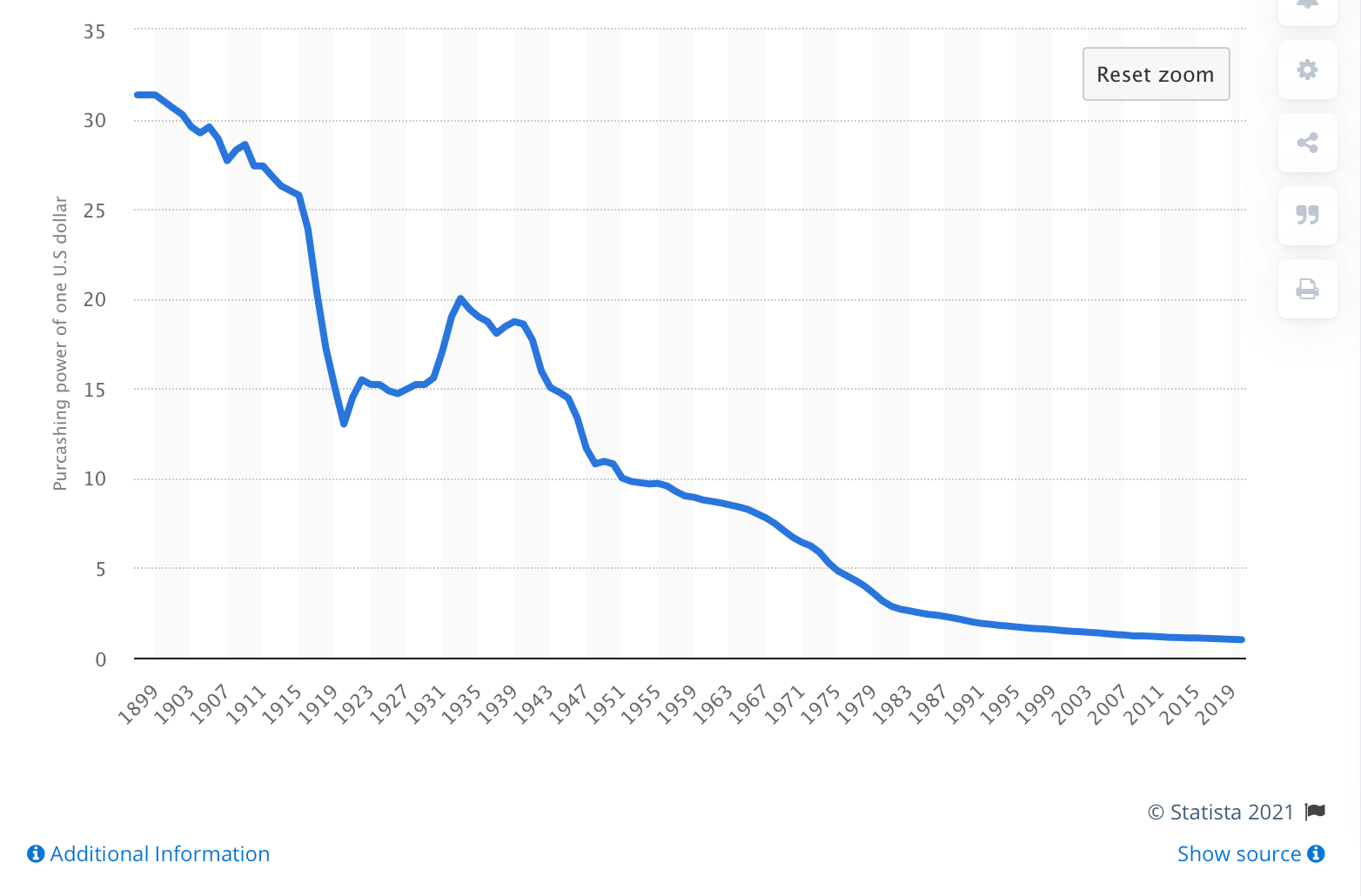

Have a look at the value of the US dollar from 1899 to present:

By doing this, the governments of the world literally rob us of our ability to save for our futures. And because they’re almost all doing it, and because there is no alternative currency, we are virtually powerless to stop them. We just have to sit back and watch as the cost of living increases year after year. Keep in mind, this is not because “prices are going up” as modern economists would lead you to believe, but in fact, because the value of your money is going down.

Oh, and by the way, the above chart does not include the estimated 12% inflation rate of the US dollar in 2020. Not to mention the long list of hyperinflated or completely defunct currencies.

All over the world, and throughout the history of the modern nation state, humanity has learned the same mistake over and over again. When governments have the ability to pay their debts by printing an endless supply of money, currencies collapse. This, many argue, is what lead to the fall of the Roman Empire, as well as the fall of the Byzantines. If you break the money, you break the society.

Frankly, it’s a miracle that the US dollar and British Pound have held on as long as they have.

2. Bitcoin is verifiably “hard money” (They aren’t making any more of it)

To fully understand Bitcoin, you need to understand one central idea:

There will only ever be 21 Million Bitcoins.

Unlike “easy money” that can be effortlessly and freely created (ehem, US dollar), Bitcoin is what’s known as “hard money.” In other words, you cannot make more of it without doing considerable work. The software protocol for Bitcoin itself has a hard-coded limit of 21 Million Bitcoins. At the time of this writing, there are 18,744,550 Bitcoins in existence, with 6.25 new Bitcoins created approximately every 10 minutes. The amount created will become smaller and smaller according to a predetermined schedule, until some time in 2140, when there will be no more Bitcoins left to create.

How can we be sure? I mean, software can be edited, right? Well, not exactly. You see, the rules of Bitcoin are enforced by every single decentralized “node” on the planet. That means that a swarm of hundreds of thousands of computers, worldwide, are all independently verifying that the rules are being obeyed. If you try to break the rules, they will reject you and any transaction you try to submit. Therefore, in order to attack the network and issue more Bitcoins, it would take more computing power — and more electricity — than even the most powerful nation-states could muster together. Or, you could try to find and take out all 300,000+ computers all over the world. Good luck with that.

What’s more, because people inevitably make stupid, easily-avoidable mistakes (like not backing up their keys) and lose access to their Bitcoin, the available pool becomes smaller and smaller, and the value for the rest of us gets higher and higher. In the words of Satoshi himself, “Lost coins only make everyone else’s coins worth slightly more. Think of it as a donation to everyone.”

Here’s the crazy thing:

In this way…

Bitcoin is literally the most scarce resource on this planet.

How can that be, you ask?

Every day, more gold and diamonds are dug out of the ground — and that’s before we figure out how to mine asteroids or other planets. Every day, new apartment complexes go up, creating more supply in the real estate market. Heck, some countries like Singapore and Dubai have even figured out how to create more land!

But not Bitcoin. Nobody — literally nobody — can create more than 21 Million Bitcoins.

3. Bitcoin is a great investment (and a solid hedge against uncertainty)

Now that you understand the fixed limit on Bitcoin, you will easily understand why it’s a great investment. In a world of infinite creation, Bitcoin is the only truly finite resource I can think of, besides time itself. With more people being born every day (and more people losing their Bitcoin keys, too), there is an ever-increasing amount of competition for an ever-decreasing number of coins.

If everyone in the world wanted to own just ₿0.1, they couldn’t. If every Billionaire in the world wanted to buy ₿10,000…. they couldn’t. There is only ₿0.00269 per person available… much less if you consider that as much as 20% of the current supply has already been lost forever (Satoshi himself seems to have “burned” an estimated ₿1,000,000 — the largest donation of any person in history). As my friend David points out…

by the end of 2021, 90% of all Bitcoin will have been mined — and only about 2% of people on earth already own some.

As more and more people understand this — understand the incredible scarcity of Bitcoin — the value can only go up. After all, they aren’t going to make any more! Fortunately, Bitcoin can be divided down to ₿0.00000001, or 1 Satoshi, so you can still buy a lovely 3,000 “sats” for just $1. What a deal!

What’s more, Bitcoin’s existence outside the traditional monetary system makes it a very powerful hedge against uncertainty. I once heard a quote: “I don’t know what weapons World War III will be fought with, but World War IV will be fought with sticks and stones.” I believe that the same is true of Bitcoin. I don’t know what the future of the US Dollar, the British Pound, the Euro, or even the countries that issue those currencies are going to be. But I do know that the Bitcoin blockchain is going to keep running no matter what happens to them. If ever the day comes that those currencies lose their value, I’ll be more than happy to accept Bitcoin in my rental properties and businesses.

I used to think that keeping 5% of my wealth in Bitcoin was enough. Today, I honestly ask myself if I’m comfortable keeping as much of my wealth in fiat and fiat-based instruments as I do. Especially when the money printer goes “brrr” nonstop…

4. Nobody “controls” Bitcoin (and nobody can)

“OK, so, wait a second. If nobody can create more Bitcoin, then, like, who controls this thing?”

This is a concept that is really hard for beginners to grasp. They often (falsely) believe that Bitcoin is controlled by the core development team (the people building and maintaining the software that runs the network) or by the miners (the people doing complex mathematical calculations to secure the Bitcoin network and process transactions). And while these people do have a say in the future of Bitcoin, they don’t “control” it. And nobody — not governments, not corporations, and not even cartels of all of the above, ever could.

This is because…

5. Bitcoin is open source, transparent, decentralized, and democratic

In reality, Bitcoin is a consensus protocol. Baked into the software is an incredible system for expressing support for and voting on changes.

Let’s say, for example, you have an idea that could improve the way Bitcoin operates — or at least, you think it could.

Great! You would then just need to submit a Bitcoin Improvement Protocol, outlining the idea and how it works. If you get enough support, you can recruit others to write it into code, which full node operators (people with entire copies of the Bitcoin network on their computers) and miners (the people processing transactions) can choose to support.

From there, voting happens every 10 minutes. Every time a batch of transactions is settled, the protocol checks to see if the miner who solved it expressed support for your idea. In order for your idea to be implemented, 90% of blocks mined need to express support for your idea. (There are other ways for everyday people who run “full nodes” to vote on and implement changes, but we won’t get into that as it’s a bit technical. Just know that even if the miners reject a change, the community can — and has — force implemented it for the good of Bitcoin).

Suffice it to say that Bitcoin is very much “the people’s money,” and unlike the changes the Fed makes every day without consent or consensus, everyday people can easily have a say in the future of Bitcoin.

6. Bitcoin is indestructible (Against just about anything you can imagine)

OK, so governments and corporations can’t control this thing… then what’s stopping them from just destroying it instead?

In reality, they can’t. Bitcoin is a completely decentralized protocol. There are no “servers” to take down — just a few hundred thousand independent computers all over the world, each of which is sufficient to keep the network alive. If you leave even one of those machines online, the network survives.

But what if the governments of the world collaborate to shut down the entire internet?

Bitcoin doesn’t care. Bitcoin is in space, running on satellites that broadcast the blockchain down to earth. In fact, it’s been demonstrated that you could even broadcast Bitcoin transactions using short-wave radio, fiber optics, infrared, or a whole litany of other impossible-to-block technologies.

Bitcoin is often referred to as “the honey badger” — because it just doesn’t give a shit. Your local currency collapsed? Bitcoin doesn’t care. The network is still running. The Iranians, North Koreans, or Martians finally muster up the courage to nuke your country? Bitcoin doesn’t care. The network is still running. In fact, short of a meteor decimating all life on this planet, it’s likely that the Bitcoin network will continue running. In fact, because so much of it is powered on renewable energy, it might even outlive us…

Fine, so the technology is impossible to screw with. But governments can just ban the use of Bitcoin, right?

That’s true. They could. But would it make much of a difference? I mean, governments all over the world have banned drugs… and last I checked, people are still using them.

What’s more, any attempt by governments to “ban” Bitcoin would be a last-ditch effort to stop us from using them. It would be an admission that their own monetary system is under threat — which would, in turn, drive people to acquire Bitcoin. And still, many people will flout the law, and hold Bitcoin anyways. Just like they held gold when it was outlawed, and made moonshine during prohibition.

Countries can opt-out of Bitcoin and shoot themselves in the foot, but short of blocking the internet, they cannot stop their citizens from using it.

7. Bitcoin is 100% Trustless (And that’s a big deal)

We don’t often think about it, but in order to use the legacy “fiat” banking system, we need to trust a whole lot of people.

Every time you get paid in cash, you need to trust that the cash isn’t counterfeit. Every time someone pays you on Venmo, you need to trust that the sender isn’t going to call up Venmo or their bank and claim that the transaction was fraud, or that their phone was stolen. This is because transactions on the legacy banking system are fully malleable — they can be changed after the fact. But that’s just the beginning. You also need to trust that your bank and Venmo aren’t going to lock your account or your funds. You need to trust that the government isn’t going to reach into your bank account and seize your assets (which they can do with one simple letter). You need to trust that a court order won’t be placed on your assets, or that the IRS won’t freeze your accounts. And of course, you must trust that they aren’t going to devalue your money… a trust that is misplaced, considering they already have.

Bitcoin is different. From its inception, it’s been 100% trustless. When you send me Bitcoin, I don’t need to know you, trust you, or even like you. All I need to do is look at the blockchain. From there, I can see that you have the funds you claim to have, and that you haven’t double-spent them or sent them to anyone else. I can also see that you’ve transferred them to me, as verified by hundreds of thousands of computers all over the world. In fact, I can even run my own full node, so that I don’t even have to trust the maker of my wallet or their copy of the blockchain to tell me that the transaction is confirmed.

After 1 confirmation, your transaction is pretty much permanent. After 3 transactions, it’s completely irreversible. How do I know? Because, again, it would take more computing power and energy than every nation state combined for you to change the history of that transaction.

This might not seem like a big deal, but it is. First, things like credit card fraud cost consumers (and businesses) almost $30 billion dollars a year. What’s more, the ability to do business with anyone, even if we don’t know their name, opens up a world of possibilities for privacy and free commerce. Gone are the days where you needed to “trust” someone to transact with them. Don’t trust… verify!

8. Bitcoin is the only property that can’t be taken away or stolen

One of the things you hear a lot about when you go down the Bitcoin rabbit hole is the idea of “self custody.” Many people are surprised to learn that there is no “customer service” in the world of Bitcoin. If you make a mistake, send a transaction to the wrong address, or lose the only set of keys to your wallet, there is no going back.

This may seem like a bug, but it’s actually a feature.

As we’ve already mentioned, with Bitcoin, there is no bank. There’s no “company” in charge. This means that you are in complete control of your Bitcoin. Unless you do something stupid (like keeping it in an exchange, sending them to the wrong address, or using a compromised device to store your keys), nobody can “steal” it from you.

Think, for a moment, about the rest of the things you claim to own. Is the same true of any of them? If someone sues you (or divorces you), the court can take away your home. If you have gold stored in a vault, a bank employee can walk away with it. The money in your bank account? …Please. The government can not only reach into your bank account, but they can actually garnish your future wages, too.

Basically, fiat money can be stolen from you before you even earn it! 😂

Bitcoin is different. Nobody can take it away from you. And if you have taken enough steps to have “plausible deniability,” nobody can force you to give it up, either.

I, for example, lost all my Bitcoin in a boating accident just last week. I happened to be transporting all of my keys and their backups at the same time, and… oops. They’re now at the bottom of the Mediterranean. I officially own no Bitcoin. Good luck proving otherwise.

But, in all seriousness, “self custody” is one of the most important steps towards self sovereignty and self determination. If you control your own, sound money, you control your own fate. This is a tremendous amount of power to put back into the hands of people, and of course, it’s also a huge responsibility.

In a world where people set their dog’s names as passwords and put them on post-it notes, Bitcoin teaches us to take our own security seriously.

It teaches us to take custody of the things that matter to us (like our savings), without relying on or trusting others. And in exchange, it gives us access to an asset that will remain with us, no matter what.

In fact…

9. Bitcoin eliminates the need for banks altogether

For the most part, a bank’s business model is this: charge you to store and use your own money, then turn a profit on that money by renting it to other people, while giving you little if any of those profits.

It’s a pretty ridiculous model, especially if you consider that a huge portion of their profits come from things like ATM fees, wire transfer fees, overdraft fees, and exorbitant credit card interest rates.

Bitcoin fixes this. With Bitcoin, you don’t need a bank to store your money. You don’t need the bank’s outdated network to send your money. And you sure as hell don’t need their god-awful security to protect your money. You effectively become your own bank.

But what about loans and interest, you ask? Well, first of all, how many of us would actually need loans if our money wasn’t subject to constant inflation (and, maybe one day, taxation)? I’d wager that it would be quite a bit less. Nonetheless, there are a number of companies cropping up who will give you low-interest loans — as low as 1% — in exchange for Bitcoin as collateral. Best of all, at the end of your loan period, you get your Bitcoin back, even if it has appreciated.

What’s more, as we’ve already learned, Bitcoin eliminates the need for “trust” — meaning that the technology itself can be used to secure collateral for loans, rather than charging high interest rates to offset the risk of default. It’s still early days, and we have no idea what type of financial innovations will come out of the power that Bitcoin offers us, but I think it’s safe to say that lending is going to be turned on its head.

10. Bitcoin is borderless

Here’s one of the best parts of Bitcoin: it’s the first of its kind, truly global currency. It is native to the internet, and nothing else. This means that it can be transmitted instantly to anyone around the world, without intermediaries. GONE are the days of paying for international wire transfers or 9% western union fees. Bitcoin is peer-to-peer — and that’s absolutely life changing if you’re one of the one billion people who depend on overpriced cross-border remittance services.

But there’s another important aspect to being “borderless,” besides sending money to people around the world in the snap of a finger… and that’s preserving your own wealth over time.

In the late 1920’s, my great grandparents were wealthy business-owners in the thriving Jewish community of Frankfurt. Do you want to guess what happened next? In those days, the only “wealth” they could transfer to their children as they shoved them onto trains to save their lives were a few pieces of jewelry. Their wealth, homes, businesses, bank savings — and their lives — were taken by the Nazis.

Bitcoin may not fix the sometimes evil nature of humans in large groups, but it fixes the monetary ramifications. Today, If you need to flee your country (or just move under positive circumstances), you can hop on a plane with 24 words on a piece of paper — or even stored in your head. Your Bitcoin, unlike your houses, businesses, gold, and bank balances, will be there waiting for you when you land.

You see, because Bitcoin exists in the blockchain (and not on your devices or bank balances), it can go with you wherever your keys go. It’s always there, in the blockchain, wherever you are, and it will stay there until you or someone with your keys decides to move it. Bitcoin therefore allows you to store and transmit wealth and value across time, borders, and regimes.

11. Bitcoin gives you privacy

I don’t know about you, but I don’t remember when exactly I opted in to having the government and the banking system know my every transaction. Of course, I have nothing to hide — but why is it, for example, that the American government demands to see all of my bank balances and transactions worldwide, even though I haven’t lived there for a decade? I am a resident of a foreign nation, paying taxes in that foreign nation — why does Uncle Sam have his nose up my ass?

But let’s forget about governments for a second, and talk about corporations. Do you really trust corporations to know your every move? Do you want Bank of America, Chase, and VISA to know everything you buy? Do you want them to know where you travel, and when? Do you trust them not to sell that information to advertisers? And do you like it that the credit bureaus and banks have a full record of every account you’ve ever had and every missed payment you’ve ever made?

Unfortunately, there is no way for you to “opt out” of this invasion of privacy — unless you want to keep your cash under the mattress.

OR, you could use Bitcoin. Not only is your Bitcoin balance private and pseudonymous, but every time you transact in your Bitcoin wallet, it creates a new address. Sending money? It sends that money, and then routes the change to a new address. Receiving money? You’ll receive it on a fresh, 1-time-use address. These addresses can never be connected to another, and they contain no information about who you transacted with or what you bought. So, while everything ispublic and traceable on the Bitcoin blockchain, as long as you don’t re-use addresses, none of it is ever linked to you, your identity, or the things you purchase.

You might think that this makes Bitcoin the perfect tool for criminals, but it could never compete with cash for that. At least Bitcoin transactions can be traced and followed — even if pseudonymously. And plus, if we were going to resist technologies just because they make it easier for criminals, we’d have to get rid of nearly every technology ever invented, from guns to the internet and everything in between.

12. Bitcoin costs nothing to store.

You might think that this privilege of super-secure, private money would cost something, right? After all, your bank charges you a $25 fee to keep your account open, and your broker a 1% management fee to manager your portfolio. Even robo-brokers charge 0.15%! But not Bitcoin. With Bitcoin, you can store hundreds of millions of dollars, without suffering inflation, and without paying any ridiculous fees of any kind. It lives on the blockchain, free, forever.

Which leads me to…

13. Bitcoin is cheaper to transfer — no matter the amount

Perhaps you’ve heard, though, that Bitcoin transactions are expensive. Or that “Bitcoin doesn’t scale” because so many people are using it.

And yes, it’s true — at peak times, an “on-chain” Bitcoin transaction on the main Bitcoin network can cost as much as $30. Most times, it averages between $0.38 and $5. This is, compared to the early days, incredibly expensive! For example, in April of 2020, someone set $1.1M worth of Bitcoin for just $0.68.

And yet, it’s still much cheaper than the legacy banking system. Let’s start with large transactions. With the legacy system, you’re looking at $15 for a domestic wire transfer, and $25 international — regardless of the size. And they limit you to $50,000, most of the time, so if you’re making a downpayment on a new house, prepare to pay that fee multiple times over. And any time a store accepts credit card, you’re actually paying 3% more, whether or not you pay by credit card, since the vendor is paying $0.30 + 2.9% and passing that on to you. For a $5,000 purchase, that’s a staggering $150! So, without a doubt, Bitcoin wins on a transaction cost basis for large questions.

But what about small transactions? After all, $0.38 is a lot if you’re just buying a cup of coffee (though that’s pretty much what the cafe is paying over the Visa network). For that, Bitcoin has something called “The Lightning Network.” It’s a second-layer on top of the Bitcoin blockchain, and it works a little bit differently. Think of it kind of like Venmo or PayPal. After all, you don’t set up a wire transfer every time you want to pay your friend for lunch, right? You use an app built on top of the “settlement layer” of the banking system. Lightning network is just like that — except it’s instant, much more secure, much more private, and virtually free (PayPal/Venmo charges 3% if you pay by credit card or pay a business).

No matter the size of the payment, Bitcoin is cheaper — and that’s before you even consider cross-border conversions. Living in Israel, I often transfer USD to ILS, paying $25 per wire transfer and hundreds of dollars in conversion fees — and that’s using the more affordable and innovative services like Wise.com. If I used the bank’s conversion rate, I’d lose even more. If I were unbanked, and had to rely on Western Union, it would be even more!

Bitcoin fixes this. Transactions on-chain can be as low as $0.06 each, and off-chain are exponentially less than that.

14. Bitcoin is faster (yes, seriously)

Another common argument against Bitcoin is that it’s “slow.” Transactions settle every 10 minutes, on average, and you might wait hours or even days for a low-fee transaction to clear. This is true, and yet, I think people who claim this are looking at the wrong comparisons.

First of all, I don’t know if you’ve ever tried to send money overseas, but it’s really slow. My “main” bank doesn’t even do foreign wires, so it takes 2–3 days to transfer to another account that does. Then it’s another 2–3 days to transfer to the overseas bank, or, if you don’t want to get screwed on the conversion rate, 2–3 days to transfer to Wise.com. From there, they’ll take their sweet time confirming it — as much as a week, before taking another day or so to send. Finally, the money lands in your foreign account — only to be held for 2–3 days till they can confirm it. All in all, you’re looking at as much as 3 weeks. Trust me, I know.

But that’s just the beginning of it, because that transaction isn’t really “settled.” When a Bitcoin transaction is confirmed, it’s confirmed forever. It may take two hours — or even two days in extreme scenarios — but once it’s settled, the funds are in your wallet forever. Compare this to a credit card transaction — which takes 2–3 business days to appear in the vendor’s bank account. But that’s just the beginning. Have you ever had your credit card stolen, only to call the credit card company and get your money back? Guess what? That vendor loses 100% of the money — and the products, if they shipped them. You can make these types of claims as far as 90 days out — meaning that the transactions are not truly “settled” at all. The same is true of PayPal and other services. You can even call and get a wire transfer reversed in many cases. But if a payment can be reversed, it’s not really settled, is it? That means that some traditional transactions aren’t really settled for as much as 90 days. By this comparison, Bitcoin’s 10–30 minute average looks pretty good, doesn’t it?

Then again, if it’s still too slow, you can always use Lightning Network, where transactions are settled, permanently, in fractions of a second. Can your bank do that?

15. Bitcoin is more convenient

Today, our phones are pretty much our command centers. They handle our calendars, our communications, and even some of our finances. Why, then, are we still using “legacy” banking systems that are not internet native? Why, in 2021, is my bank still asking me to come in to a branch to perform certain transactions or open an account?! Why am I still carrying around credit cards, debit cards, and cash? “Do you have Cash App? PayPal? Venmo? Cash? Zelle? Do you take credit cards?” Ugh. Why do I need to manage so many different channels? And why, for god’s sake, do I need to type in account numbers or other details?

On Bitcoin, all transactions are treated the same, whether they’re large or small. You might choose to transact on Layer 1 or on Lightning Network, but the experience is still the same. Instead of typing in my friend’s account number, phone number, or whatever number, I just scan a QR code. I click “send,” and boom! The money shows up on their side. And unlike other solutions like Venmo or PayPal, once it’s there — it’s there. No additional account to manage, and no need to withdraw funds to my account, because the transaction layer is the settlement layer (at least for on-chain transactions. For lightning, you can keep them in your Lightning wallet or transfer them to an on-chain wallet if you like).

There are no account numbers to remember. No need to add someone to your contacts. No need to sign up for a bunch of services. No need to deposit or take out cash at the ATM. Just scan, click, send. Simple!

This is especially true when you compare Bitcoin to the only other thing that’s ever come close to “hard money” in human history — gold. Gold is a really great store of value, and very inflation-resistant, but it’s notoriously difficult to divide, send, carry, and secure. I’ll stick to Bitcoin.

16. Bitcoin is the future

When you really look at it, it’s not possible for the legacy banking system to continue business as usual in a fully digital and connected world. There are too many intermediaries. Too many middlemen. Too many boundaries. The system is completely fragmented by country, by bank, and by payment layer. My Zelle + Chase account can’t send to your Venmo / CapitalOne Account, much less your Wise / Lloyd’s Account, your Remitly + HSBC account, or your Payoneer + Whatever account. And even if it could, it would be expensive, between foreign transaction fees, conversion fees, transfer fees, withdrawal fees, and probably even fee-payment fees. The entire system is a mess. A slow, expensive, and archaic mess.

Bitcoin is not only the first universal, international currency. It’s also the world’s first internet-native currency.

Created by the internet, for the internet, it is a payment system designed for a world without borders or friction. Information moves freely today — why wouldn’t money?

If you look objectively at Bitcoin versus the legacy banking system, you’ll come to the same conclusion: it’s headed the way of the telegram and the fax machine.

17. Bitcoin is fair (The rules are the same for everyone).

One of the things I hate the most about the legacy banking system is just how incredibly unfair it is. Consider this, for example: as someone with a high credit score, I have access to products that many people don’t. I can get credit cards with awesome perks and cash-back rewards, sign-on bonuses, miles, and a huge line of credit right when I sign up. I can get “premium” bank accounts which pay higher interest rates and charge lower or zero fees for many types of services. Even when I do get charged a fee, I can just pick up the phone, call the bank, and get that fee waived instantly. Plus I get better access to and lower interest rates on loans. Banks are essentially chasing me down to try and recruit me as a customer, throwing an endless supply of money and perks my way, even though they make less money off me, since I never carry a negative balance or take out loans besides mortgages.

Compare this to someone who wasn’t born into a privileged, white, middle class American family. Assuming they are banked (a big assumption), they have a very different experience than I do. They pay higher interest rates, get access to inferior products, and have less access to capital. What’s more, the bank is constantly doing everything in its power to charge them fees wherever possible. How is this fair, that the people with the least money are paying the most and getting the least?

Oh, and don’t even get me started on the idea of banks being bailed out every time their own irresponsible behavior gets them in trouble. Or hedge fund managers playing by their own set of rules.

Bitcoin doesn’t operate like this, because Bitcoin doesn’t know (or care) who you are.

To Bitcoin, you are just the holder of a set of keys. Those keys may have ₿0.001, or they may have ₿1,000,000. Either way, the protocol is not going to give you any sort of preferential treatment. It’s not going to give you access to features that other people don’t have, charge you fees because you don’t have enough, or give you better transaction rates because of how much you’re worth. Bitcoin is the great equalizer: no matter how much you have, you have the same access and experience as everyone else. Plus, whenever the system improves, those benefits are rolled out equally to every single user on the network.

Which is a lovely segue into…

18. Bitcoin is hope for billions of unbanked

At this point, you might be thinking… “hey, this Bitcoin thing is starting to sound pretty good.” But let me blow your mind a little further: you are probably not the target audience for Bitcoin.

The real target audience for Bitcoin is the 2–2.5 billion people who are unbanked or underbanked — including an estimated 50 million Americans.

These are people who have access to mobile phones, but no way to safely store their money. They’re people who are forced to rely on predatory check cashing and remittance services that take as much as 10% of their earnings to perform a simple service. The other real target audience for Bitcoin is the billions of people worldwide living under fiscally irresponsible regimes who devalue and debase their currencies. Places like Zimbabwe, Venezuela, and Argentina, to name just a few. Also, Paraguay, Iran, Vietnam, Cambodia, Indonesia, Brazil… need I continue?

For you and I, Bitcoin is an incredible new technology that will give us incremental value and convenience compared to our existing monetary instruments. We don’t really NEED Bitcoin. But for these individuals, Bitcoin is hope.

It’s a way out of a broken system that has impoverished them and wiped out their savings generation after generation. It’s an on-ramp to joining the global economy, with a currency that holds its value, crosses borders, and is increasingly accepted everywhere.

Sure, you and I can argue the merits of Bitcoin, the challenges it faces, and the future potential of the technology. But billions of people don’t have that luxury. For them, Bitcoin is the only way out.

19. Bitcoin is fully permissionless

So how can Bitcoin succeed where legacy banking (and central banking) have failed? I mean, over 2 billion people have been marginalized by this system — there’s no way that some geeky, open-source money from the internet can do any better.

Oh, but it can, it will, and it is!

You see, to join Bitcoin, you just have to download a wallet and open an app. You don’t even need to be online continuously (though most of the “base of the pyramid” do have access to mobile data today).

There is no ID verification. No sign up process. No approvals. Nothing. Bitcoin is completely permissionless, both as a user, and as a developer.

That means that I cannot stop you from using it — and you cannot stop me. You cannot force me to use a specific wallet, either. Just look at El Salvador, which is airdropping $30 worth of Bitcoin (now legal tender) to each of its citizens, but only if they want to use the official wallet app. They’re free to use any wallet they want — and so are you. You can open as many wallets as you want, move your funds as many times as you want, move from one wallet software to another by restoring your keys, and more. And most importantly, you can now save your money in an asset that appreciates. At no point in any part of this process do you need permission or approval.

That’s a really big deal if you are unbanked.

Which leads us to…

20. Bitcoin is completely censorship resistant

When you join the Bitcoin economy, a few things will probably stand out to you. First of all, you’ll likely realize that “your” money is “yours” in name only (and, quite frankly, hardly “money” at all, but a system of IOUs — but that’s besides the point). In order to actually use your own money, you need to ask permission. You need approvals. And guess what? Your bank doesn’t have to give you those approvals.

Don’t believe me? Just try the simple act of transferring money into a Bitcoin exchange. After all, it’s your money, isn’t it? You should be allowed to do whatever you want with it. But no. The legacy banking system has decided for you that they want to “protect” (prevent) you from getting mixed up in this cryptocurrency thing. Depending on the bank, they’ll block your transaction — or even close your account.

Now, if you think that was hard, try sending some money to that freelance software developer you’ve been working with in Tehran. Or donating to Wikileaks. Or even just sending a donation to a new charity organization in Gaza.

You can’t. Because the legacy banking system will censor you. They will block your ability to transact. And while I’m the last person who believes it should be easy to fund terrorism, you have to ask: do they really need to have this power over us?

Governments already have a monopoly on the use of force, and unprecedented ability to surveil us online and in the real world — shouldn’t that be enough for them to combat terrorism, money laundering, and fraud? Do they really need to block my $20 donation to a family in Syria?

21. Bitcoin reduces government control

As you’ve probably gathered by this point, Bitcoin is pretty anti-establishment. Born out of the cypher-punk movement, freedom is part of its very DNA. (As my friend Ari points out, this is kind of ironic, considering the NSA invented the SHA-256 encryption algorithm that it uses!)

We’ve already talked a bit about how Bitcoin reduces the government’s ability to censor, confiscate, or monitor your finances — but it goes much, much further.

Governments all over the world manipulate the economy, and the lives of their citizenry, by manipulating the money. This isn’t some crazy conspiracy theory — it’s the basis of Keynesian economics and the central banking system as a whole. The government, in all their wisdom, tweaks levers such as interest rates and money supply to try and get the economy to stabilize, without acknowledging that the real problem in most modern economies is what they call “quantitative easing” — i.e. they just can’t seem to stop printing money.

This control extends far beyond unemployment rates and inflation, into geopolitics. Wars are funded by governments with the power to print an endless supply of money. It’s the reason that World War I grew from a small, regional conflict to a multi-year global disaster (As Saifedean Ammous explains in The Bitcoin Standard, governments at the time suspended the Gold Standard to print more money out of thin air and fund their militaries). If the government couldn’t print money, they’d have to pay for wars through taxation alone — and they’d need voter support to do it. How many wars do you think would have been avoided if they had to be supported by the majority of voters enough to pay out of pocket?

Bitcoin changes all that. The money supply is fixed, and it’s value is determined by supply and demand. This means that the more citizens all over the world transition their wealth away from fiat currencies and into Bitcoin, the less power the government-backed fiat currencies have, and the less power their purveyors have as a whole.

I’m not anti-government by any means. I rather like having healthcare, a police force, and a system of law. But I do wonder: it took centuries for us to come out of “the dark ages” with the understanding that the state and religion should be separate. How long will it take for us to realize that the same is true of our money?

22. Bitcoin is more environmentally friendly (Yes, you read that right)

Speaking of war and governments, I want to take a moment to touch on the big “environmental” concern of Bitcoin, with a couple of thoughts.

You’ve probably heard that Bitcoin consumes a ton of energy — as much as some nation-states — and that’s true. Sure, an increasing percentage of that energy is renewable, carbon-free (a recent report from the Bitcoin Mining council states 54%), or otherwise wasted, but that’s actually besides the point. The question is, what is the alternative, and what do we get in exchange?

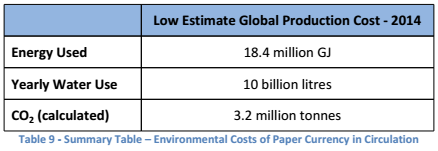

Comparing Bitcoin to the legacy financial system is revealing. Just the printing of paper money alone consumes a tremendous amount of electricity — and fresh water — while producing millions of tons of CO2:

But that’s just a fraction of the energy used to run the “fiat” monetary system. You then have to factor in all of the banks, which consume an estimated 100 terawatts of energy per year to power their servers and offices. That’s twice as much as the entire Bitcoin network!

But it doesn’t end there. Because you then have to consider all the ancillary energy use and CO2 emissions that prop up the fiat monetary system. How much are countries spending in defense and military budgets to secure their economies against cyberattacks? How much military spending are fiat currencies financing with their endless ability to print money? How much are countries worldwide spending to convince us that “the full faith and credit” of their government is actually worth something?

If I were to flip a switch, right now, and replace the legacy financial system with global adoption of Bitcoin, I bet we could save hundreds of millions of tons of CO2 every year.

But that’s still not the point. Because, you see,

even if Bitcoin consumed more energy than the legacy banking system — it would be worth it.

Just look at all of the problems Bitcoin is solving. Poverty. Inflation. Remittance. Fraud. Security. Economic disenfranchisement and discrimination. Privacy. Look at how many people Bitcoin can (and will) lift out of poverty. If all Bitcoin did was provide us with sound, borderless money, it would be worth it — especially if you ask someone who has lived their entire life unbanked and on hyperinflated fiat money. After all, money is the foundation of our entire society. Money — as a tool for collaboration — is the reason why we as a species are enjoying such unprecedented peace and prosperity. If better money isn’t worth the energy expenditure and carbon emissions, then what the hell is?

23. Bitcoin is a hotbed of open-source innovation

Over the last couple of decades, the banking industry has given us very few real innovations. You have a card. You can tap the card instead of swiping it, or connect it to your phone to pay your friends. Big. Freaking. Whup. The realinnovations, the banking industry keep for themselves. Innovations like algorithms that reorder your transactions so that you get charged more overdraft fees. Or innovations like the types of shitty financial derivatives that caused the 2008 global financial meltdown. They’re an innovative bunch — just not in the right ways.

Bitcoin, on the other hand, is different. Because it’s permissionless and open-source, anyone and everyone can innovate for it. You can build apps on top of it that solve new and novel problems. No applications, approvals, or permissions required. And, for the most part, everything that’s being built is open-source. Nobody can trick you into paying fees you don’t anticipate, because you can examine the code yourself. And if you don’t like that code, you can write some better code yourself.

This is why Bitcoin is innovating and improving at a break-neck speed. Multi-signature wallets. Taproot. Schnorr Signatures. Lightning Network. Smart Contracts. Decentralized Exchanges. You might not know what any of that means, but these are all incredible innovations being built, open source, on the Bitcoin blockchain. And it’s all happening incredibly quickly.

Which leads me to…

24. This is just the beginning for Bitcoin.

The best metaphor to help people understand this comes from Andreas Antonopolous, a thought leader who has converted millions of Bitcoin acolytes all over the world. He reminds us that Bitcoin today is roughly where the internet was in 1997 or 1998. We could have never imagined things like Zoom, Netflix, Oculus VR, or Facebook Live back then. We could have never imagined we’d be turning on our lights, watching our nanny cams, and unlocking our doors over the internet from miles away. All we saw was email and basic web pages.

Similarly, we have no idea what will be built on Bitcoin over the next 20 years. It’s still early. But the potential has already demonstrated itself to be immeasurable. As Andreas likes to remind us, Bitcoin isn’t just “the money of the internet,” it’s also “the internet of money” — and payments is just the first application, like email was for the internet. And yes, there were plenty of people who said that the internet was a geeky fad, too.

You might feel like you’re “too late” to get involved, but you’re not. It’s still 1997 on the Internet — and you are still one of the first 200 million people to get into Bitcoin.

It’s a deep rabbit hole, and there is a lot to learn and unlearn — but it is well worth it. After all, this is universal human freedom — economic and otherwise — that we are talking about here.

— –

I hope that this article has inspired you to take a deeper look into Bitcoin and it’s potential.

If it has, make sure to follow me on Twitter @jonathanalevi and consider subscribing to my upcoming YouTube channel. And if you’re ready to go deeper and take the orange pill, check out my Bitcoin MasterClass, which will teach you the ins and outs of safely buying and holding Bitcoin.

Keep HODLing

JL